Will Luckin Coffee Be Listed Again

Robert Way/iStock Editorial via Getty Images

Investment Thesis

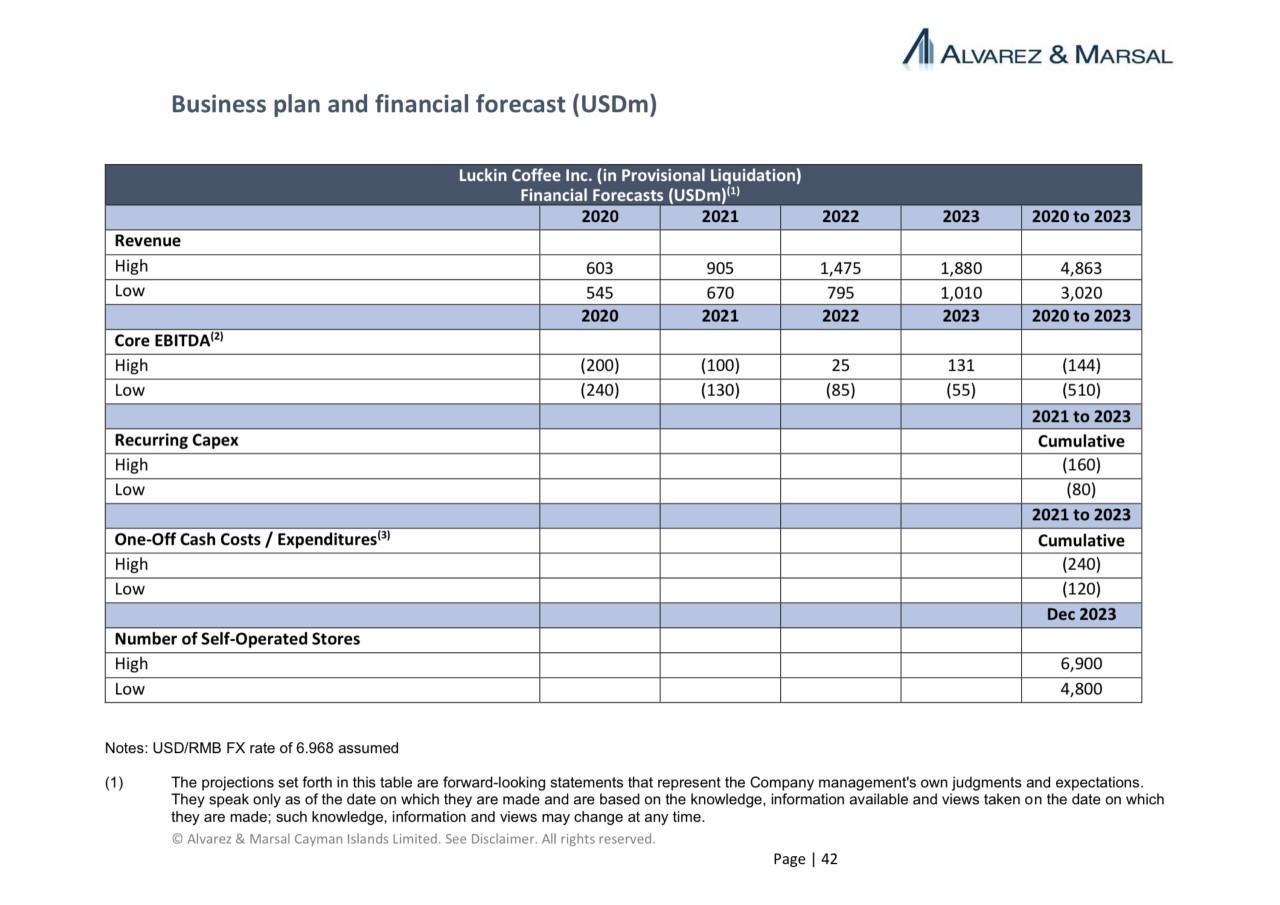

Since our last writeup was published in August 2021, Luckin Coffee Inc. (OTCPK:LKNCY) has successfully addressed all the issues related to the accounting scandal while maintaining positive momentum of its cadre concern, notwithstanding its stock has drifted substantially lower, trading at only 2X Price to Sales (P/Due south) and $0.five 1000000 per store.

We believe that this deep valuation gap vs its peers is not sustainable and a relisting to a main commutation is imminent. Upon a successful relisting, LKNCY'due south stock will have at least 3x upside from the current level fifty-fifty assuming a discount for ADR delisting concerns.

Valuation

We have updated LKNCY'due south valuation analysis with the latest information. Non surprisingly, it remains significantly undervalued based on both the trading multiple and per store valuation. Its P/S ratio has compressed over l% during the past 8 months due to higher acquirement and a lower share price. Its per store valuation too has dropped by half during the same period as the company has opened more new stores on a net basis while the marketplace capitalization has shrunk.

LKNCY released its 2021 unaudited financial results on March 24 th, 2022. Its full twelvemonth revenue in 2021 was up 97.5% from last yr to $ane,249.9 million which is besides 38.ane% higher than the loftier end of the visitor's forecast range for 2021 in the JPLs beginning report (see table below).

JPLs first report.

Source: JPLs first report.

If we use 2021 actual revenue and a projected growth charge per unit of 63% in the same JPL report, LKNCY would generate a acquirement of $2,037.3 million in 2022. As of April ane, 2022, LKNCY's market place capitalization was $2.3 billion, implying a P/Due south ratio of 2.0x for 2021 and 1.3x for 2022. All of its manufacture peers trade at a significantly higher P/S multiple (meet table below).

Price/Sales Multiple

Companies Market Cap Price/Sales Starbucks (SBUX) $105 billion 3.6x 2021 Sales iii.2x 2022 Sales Dutch Bros (BROS) $9 billion 18.9x 2021 Sales 13.2x 2022 Sales Tim Hortons China (SLCR) $2 billion 17.9x 2021 Sales 7.6x 2022 Sales Luckin Coffee Inc (OTCPK:LKNCY) $2 billion 2.0x 2021 Sales 1.3x 2022 Sales

Notes: The trading multiples are as of April 2, 2022 except SLCR which is calculated based on the info of its contempo SEC filing.

On per store basis, LKNCY is also undervalued past a very wide margin compared to its publicly traded comparables. It is worth mentioning that the store count of LKNCY has now surpassed SBUX which has over 5,500 stores in Communist china, but valuation per LKNCY store is simply one sixth of a SBUX shop.

Per Store Valuation

Company # of Stores* Market Cap ($ bn) Valuation ($ mm)/Store Starbucks (SBUX) 34,317 $105 $three.ane Tim Hortons Cathay 410** $1.ix $4.6 Nayuki Tea (2150 HK) 817 $1.0 $1.iii Luckin Coffee (OTCPK:LKNCY)*** 4397 (only cocky-operated stores) 6024 (including partnership) $ii.iii $0.v $0.4

*Number of stores in Communist china except Starbucks which is worldwide store count.

**Visitor store count as of 1Q 2022

***LKNCY shop count is as of December 31, 2021

Source: Bloomberg.

Based on these two valuation methods, we are still of the view that the valuation gap will near likely exist airtight past a relisting onto the master exchange. LKNCY stock cost could have at to the lowest degree 3x upside from the current level and we would not be surprised if it rallies 5x given the current price discount confronting its peers.

Relisting or Delisting

With both legal and restructuring issues well addressed, relisting is the adjacent cardinal catalyst to close LKNCY's valuation gap with its comparables. We still believe that the company will seek a relisting on one of the main US exchanges, most likely the NASDAQ, every bit information technology would be more difficult and time consuming for a company with a tainted history to get listed in either mainland China or Hong Kong.

As well since the company is currently majority-owned by a individual equity firm, it is reasonable to presume that the private equity business firm will demand to generate a positive IRR during 2022 from this big position (hint: fees). Relisting volition certainly aid accomplish that goal with huge blastoff potential. Some other motivation factor that we had mentioned in our writeup final twelvemonth, is that per an article in the Wall Street Periodical, the fund had to put its $2.5 billion new raise on hold after the untimely LKNCY blowout. The eventual turnaround and a successful relisting of LKNCY volition regain the credentials the fund needs to relaunch its paused capital raise.

Unfortunately, relisting has recently been overshadowed past the delisting concerns for all Chinese ADRs. We believe the delisting overhang is mode overblown and has actually created a skillful buying opportunity for LKNCY. The reasons are equally follows:

i) Solution is on the manner. According to a recent Bloomberg written report, The China Securities Regulatory Commission (CSRC) and other national regulators are in the process of drafting a framework that could potentially permit the U.S. regulators full access to inspect papers of most Chinese ADRs as early as mid-twelvemonth. Though there are nevertheless uncertainties on whether this volition eventually materialize, delisting should no longer exist a significant overhang for LKNCY anymore.

ii) LKNCY is not an intended primary target. LKNCY is currently still an OTC listed company and should not be the primary target of delisting which seems to focus more on the get-go tier ADRs listed on the NASDAQ and NYSE.

3) LKNCY is more than ready and capable of handling delisting-related auditing compliance to avoid the delisting. Even if the OTC listed Chinese companies were too included in the delisting review, in theory LKNCY should be more than set up and capable of treatment the delisting related compliance procedure and not beingness delisted given that information technology just successfully completed a more complicated and rigid courtroom-mandated forensic investigation as a issue of its accounting scandal.

4) Forced delisting driven by political tension is possible but a very depression probability. Though delisting should exist a regulatory process, more than recently it is as well driven by geopolitical factors. Even if the auditing requirement is met, the The states government can even so delist a United states listed Chinese company for political reasons with a contempo example being China Mobile. That said, it will take a full blown bilateral confrontation and subsequent indiscriminate delisting (even OTC listed companies) past the authorities for LKNCY to be really impacted. That would be a very low probability outcome.

Accelerated New Store Opening

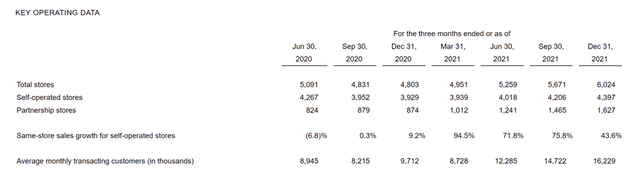

In the press release dated March 24 th, 2022, LKNCY as well disclosed the key quarterly operating information till the end of 2021 (run into tabular array below).

Company filing

Source: Company filing.

Further analysis on the data shows the following trends:

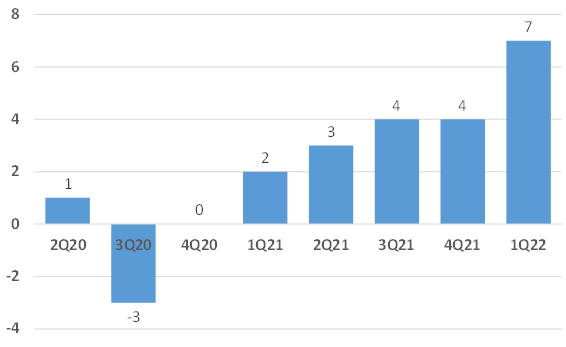

1) The step of new store opening has accelerated over the last iv quarters. Immediately after the accounting scandal, LKNCY suspended new shop opening and actually closed some underperforming stores. No cyberspace new stores were opened until the showtime quarter of 2021. The pace of new openings, measured by boilerplate new store openings per twenty-four hour period, has jumped from ii per day in 1Q 2021 to 4 per day in 3Q 2021 and further to 7 per twenty-four hour period in 1Q2022 (run into chart beneath).

Average New Shop Openings per Mean solar day

Company filing and wechat channel

Source: Visitor filing and webchat official channel.

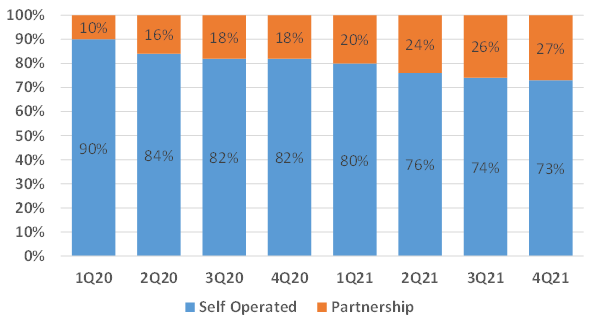

2) Partnership stores have been taking an increasingly higher share in the total store mix. LKNCY has two types of stores, self operated stores and partnership stores (i.e. franchised stores). The partnership stores are typically located exterior the beginning and 2d tier cities, which used to exist LKNCY'south core markets for growth. As the core markets became saturated, the company started to shift its focus to the 3rd and fourth tiers cities via opening franchised stores to minimize the capital letter outlay. Partnership stores have increased from 10% of the total stores in 1Q 2020 to 27% in 4Q 2021, i.due east. almost 3X in two years (see chart below).

Partnership Stores as % of Total Stores

Visitor filing

Source: Company filing.

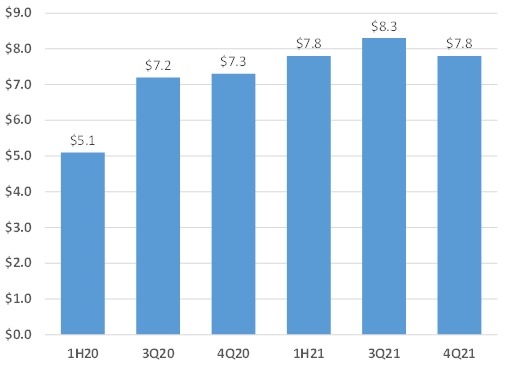

three) Average revenue per transacting customer (ARPTC) has been steadily increasing. We derive the number simply by dividing the quarterly revenue by average monthly transacting client number*iii. This could be a good proxy for average ticket size per customer. During the 18 months from the end of June 2020 to twelvemonth-end 2021, ARPTC increased 53% from $5.i to $7.eight (see chart below). We have to admit that this is Not the most ideal method as the calculation assumes that each transacting customer but fabricated i transaction per month for three months, but it is good enough to cheque the growth tendency.

ARPTC Growth Chart

Company filing and wechat channel

Source: Company filing.

To keep ARPTC of $vii.8 (equivalent of l Yuan in local currency) in perspective, we have asked our local contact in China to check what 50 Yuan could buy in a Luckin store. It turns out quite a lot, including one of its most pop drinks - coconut latte, 1 ham cheese croissant, one greenish tea cheesecake, 1 tiramisu block, and ane mocha carmine bean roll (see screenshot below).

What 50 Yuan Can Buy at Luckin Store

Visitor mobile app

Source: Visitor mobile app.

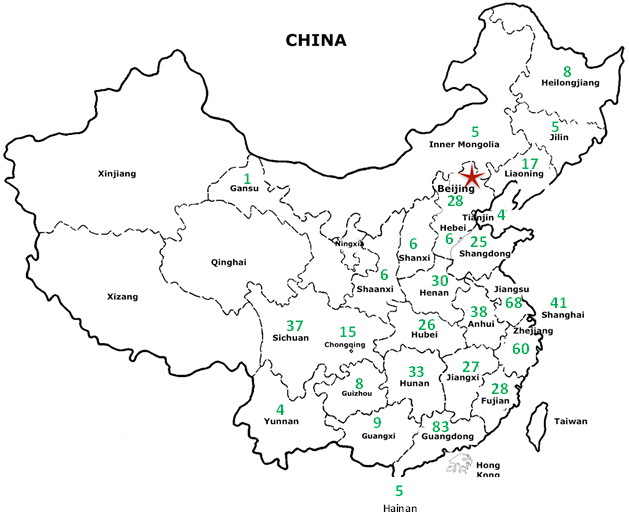

Every calendar week LKNCY releases a new store opening update via its webchat official aqueduct which includes the number and location of the new stores opened during that week. We aggregated all 1Q 2022 weekly new shop opening data and then grouped them past province on a map of China (see below). Ane primal ascertainment from this exercise is that during 1Q 2022 LKNCY has opened new stores in virtually all the Mainland provinces except four (Xinjiang, Tibet, Qinghai and Ningxia) which is understandable as all four have very unique local drinking habits due to cultural and religious reasons. This "total coverage" approach is consistent with the visitor's strategy to focus future growth more than towards the third and lower tier cities as the top tier cities are getting saturated and more than competitive.

New Stores Opened in 1Q 2022

Visitor filing and wechat channel

Source: Company wechat official aqueduct.

What the map could not prove is the new store breakdown by the urban center tiers. The cities in China are divided into five tiers based on several factors such every bit geographic size, Gdp, population etc. The tiers are as follows:

1) 4 first tier cities: Beijing, Shanghai, Guangzhou and Shenzhen

2) fifteen new get-go tier cities: Chengdu, Chongqing, Hangzhou, Wuhan, xi'an, Zhengzhou, Qingdao, Changsha, Tianjin, Suzhou, Nanjin, Dongguan, Shenyang, Hefei and Foshan

3) 30 2nd tier cities

4) 70 3rd tier cities

5) 90 4th tier cities, and

6) 128 5th tier cities

The table below regroups the information by these urban center tiers and shows that 45% of LKNCY 1Q 2022 new openings are in 3rd or lower tier cities. Nosotros would assume that the bulk of the stores in those 45% are partnership stores, i.e. shares of the partnership stores in the total mix at the end of 1Q 2022 is highly likely to exist college than 27% at year-end 2021.

LKNCY New Store Openings by Cities

Number of New Stores in 1Q 2022 % of Total First Tier Cities 88 15% New First Tier Cities 127 21% Second Tier Cities 114 19% Third, 4th & Fifth Tiers Cities 264 45% Total 593 100%

Source: Company wechat official channel.

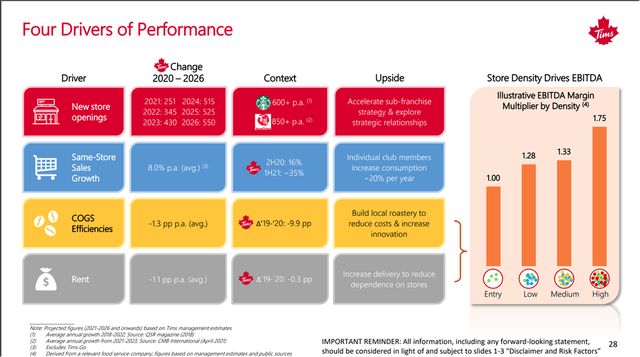

How volition the accelerated store opening touch on LKNCY'southward financials? Tims Prc (SLCR) shares a very practical framework (slide 28) in its investor presentation: iv drivers of performance (see the graph below).

Tims Prc Performance Drivers Framework

Visitor filing

Source: Company filing.

The 4 drivers are new shop openings, aforementioned store sales growth, COGS efficiencies and rent, essentially two top line growth drivers and two cost drivers. Using LKNCY 2021 full year financials equally an example (see table below), why was the acquirement up 97.five% from 2020 while shop units "but" increased by 25.4% during the same period? The reply is growth in average monthly transacting customers, i.e. 55.two%. We can simplistically guess the revenue growth by using the post-obit formula (1+25.4%)*(one+55.two%)-ane =94.vi%. The actually growth is 97.5%, close plenty. We can also apply same stores sales growth for this practice, but since the disclosed number is for self-operated stores, it may inflate the guess.

LKNCY 2021 Top Growth Highlights

Store Unit YoY Growth 25.4% Same Store Sales Growth (Self Operated) 69.iii% Average Monthly Transacting Customers YoY Growth 55.two% Revenue YoY Growth 97.v%

Source: Company filing.

We can apply this forecast method to 1Q 2022. LKNCY'south shop unit sequential growth is 10% and if we presume that average monthly transacting customers growth is x%, the aforementioned as the 4Q 2021 level, the full revenue could exist upwards 21% sequentially from year-terminate 2021. And at this pace, the total year revenue could be potentially upwardly at least fourscore%. Over again, this is merely a dorsum-of-the-envelope blazon of guess of the potential touch on of new store openings, should not exist a basis for investment decisions.

Key Risks

ane) COVID lockdown in China. This is a articulate and present risk as this Omicron outbreak has already locked downwardly Shanghai, the largest city in China. This will certainly negatively impact LKNCY'due south business, though it should exist just a temporary hit. During 1Q 2021, several cities were partially locked down due to the Delta outbreak, and LKNCY'south average monthly transacting customers dropped by 10% sequentially, but immediately bounced back after lockdowns were lifted and were upwards twoscore% in 2Q 2021. Another natural mitigation for LKNCY is that a majority of its revenue is from commitment which tin can still operate during a lockdown as long as delivery platforms such as Meituan remain operational.

two) An economic slowdown or recession in China. If either happens (well-nigh probable will), LKNCY volition be hurt due to shrinking consumer spending. However, it is highly probable that the Chinese government will accept to start a new round of stimulus measures, including interest rate cuts and spending coupons which basically gives cash straight to the consumers, etc. The Shanghai lockdown volition just accelerate the release of these stimulus measures. So any negative impact for LKNCY from the upcoming slowdown could be softened by these stimulus measures.

three) Cathay regulatory risk. One of the potential regulatory risks for LKNCY could be information security as the company will handle a lot of the consumer data on a daily basis. Tims Prc has prepare an example to address this business past setting up an contained company to safeguard the data security and to be in compliance of whatever related regulatory requirement. We practice not see this equally a big risk for the visitor's relisting process.

Determination

For LKNCY, the only event we are waiting for at this point is the relisting. The stock is currently deeply undervalued and a successful relisting will be the goad to shut the valuation gap. The delisting overhang on Chinese ADRs is more than dissonance than reality, especially for LKNCY, which is still OTC listed. The potential upside of LKNCY is at least 3x from the current level.

This commodity was written by

Sharing ideas on warrants, SPACs, capital construction arbitrage and event driven opportunities. Non fiscal advice. Quick comments and updates are posted from time to time on Twitter www.twitter.com/BuffetWarrant.

Disclosure: I/we accept a beneficial long position in the shares of LKNCY either through stock buying, options, or other derivatives. I wrote this article myself, and it expresses my ain opinions. I am not receiving compensation for information technology (other than from Seeking Alpha). I accept no business relationship with any company whose stock is mentioned in this article.

whiteleggespeargons.blogspot.com

Source: https://seekingalpha.com/article/4500579-luckin-coffee-relisting-delisting

0 Response to "Will Luckin Coffee Be Listed Again"

Post a Comment